Discover Financing Options for Your ADU Project in Connecticut

Discover Financing Options for Your ADU Project in Connecticut

ADU financing helps Connecticut homeowners pay for the design, permitting, site work, utilities, and construction of an accessory dwelling unit.

Whether you want to build a private small home on your property for a parent, create an in-law suite, add rental income, or plan for future downsizing, the right financing strategy can make the project more realistic.

In Connecticut, financing an ADU is not just about choosing a loan. Your town rules, lot layout, setbacks, septic or sewer setup, survey status, utility distance, and total project scope can all affect the best path forward.

That is why many homeowners first want to know what is possible on their property, what the full investment may look like, and whether the monthly payment can work for their family.

For many Connecticut ADU projects, a planning range of $150,000 to $300,000+ is common depending on size, finish level, site conditions, utility needs, permitting, and whether the unit is attached, detached, or built inside an existing structure.

The right ADU financing option can help you move forward with more clarity instead of guessing, delaying, or giving up too early.

What Is ADU Financing?

ADU financing is the process of using a loan, home equity, refinance, renovation loan, construction loan, or other funding source to pay for an accessory dwelling unit.

It is different from a traditional home loan because an ADU is often a new living space that does not exist yet. A lender may need to look at your current home value, available equity, estimated project cost, after-repair value, builder scope, and how the ADU will be used.

In Connecticut, ADU financing can also be affected by town-specific zoning and valuation challenges. One town may allow a detached ADU, while another may have different rules for size, placement, parking, owner occupancy, or short-term rental use. A homeowner may also need to consider septic capacity, utility connections, wetlands, slopes, driveway access, or whether a current survey is available.

That is why financing an ADU should not start with a generic loan quote alone. It should start with your actual property, your actual use case, and a clear understanding of what is included, what may be extra, and what steps are needed before construction.

ADU Financing Options in Connecticut

Home Equity Lines of Credit (HELOC)

Tap into the equity of your home to fund your ADU with manageable monthly payments

A custom accessory dwelling unit (ADU) allows you to design a space that perfectly meets your needs, whether it’s for rental income, multigenerational living, or a personal retreat. With a custom ADU, the possibilities are endless.

Lower Rates

Compared to alternatives such as personal loans and credit cards

Fast Funding

Full draw up front with funding in as few as 5 days!

100% Online Application

No need to go to the bank; apply from the comfort of your home

Up to $400k

1st, 2nd or 3rd lien positions with terms of 5, 10, 15 or 30 years!

See Your Rates In a Few Clicks

Without impacting your credit score!

Alternative Lenders We Recommend

HELOCs, Personal Loans & Construction Loans

Up to $500k with terms of up to 30 years and competitive rates

Secured & Unsecured Personal Loans

Up to $100k with terms of up to 12 years

One customer that comes to mind was a daughter who wanted to build an ADU in her backyard for her aging mother. She had some equity in her home, but not enough to finance the full build through traditional lending. Her mother planned to sell her home and use those proceeds to pay for a large portion of the project, but they did not want to sell before the ADU was complete. The solution was a renovation HELOC against the daughter’s property. Because a renovation HELOC can factor in the property’s future post-construction value, the family was able to move forward with the ADU before listing the mother’s home. Once the home was sold, the proceeds were used to pay down the HELOC, leaving a smaller balance that could be paid over time. For homeowners who think they may not be able to finance an ADU, it is always worth discussing the options. Even if now is not the right time, it is important to understand the actionable steps that can put you in a position to build in the future.

Cash-Out Refinance

Reinvest in your property by refinancing your mortgage for your ADU project. A cash-out refinance replaces your current mortgage with a new, larger mortgage. The difference between the new loan and your existing balance can be used to help fund your ADU.

This may make sense if your current mortgage rate is close to available market rates, if you want one long-term mortgage payment, or if you prefer a fixed structure over a separate line of credit. It may be less attractive if your current mortgage has a much lower rate, because refinancing the full balance could increase your total borrowing cost.

For Connecticut homeowners, a cash-out refinance should be compared against a HELOC, renovation HELOC, and construction loan before deciding.

Renovation & Construction Loans

If you don't have enough equity in your property, a Construction Loan can bridge the gap by tapping into the future equity of your property with the added ADU.

A renovation loan or ADU construction loan may be based on after-repair value, also called ARV. This means the lender may consider what the property is expected to be worth after the ADU is complete, not only what it is worth today.

That is the key difference between a construction loan and a standard HELOC. A standard HELOC usually depends on current equity. A renovation or construction loan may consider future value, project plans, builder scope, and the completed property appraisal.

This can help Connecticut homeowners who have a strong ADU plan but not enough current equity to cover the full build.

Shared Equity Financing

Shared equity financing may allow a partner or lender to help fund the ADU in exchange for a share of future profit, rental income, or property appreciation.

This option can reduce the need for traditional monthly payments, but it also means giving up part of the upside.

Before choosing this route, review repayment terms, buyout options, sale triggers, rental income expectations, and long-term ownership impact.

ADU-Specific Loan Programs

Reinvest in your property by refinancing your mortgage for your ADU project.

This program can help eligible borrowers finance the purchase or refinance of a home, along with qualified rehabilitation costs through one mortgage. For ADU buyers, this may be relevant when the project involves renovating, improving, or adding living space as part of an eligible FHA-backed renovation loan.

Fannie Mae allows certain mortgage products to be used for homes with ADUs, renovating an existing ADU, or adding an ADU to a borrower’s existing home. This may be useful for Connecticut homeowners who want to finance an ADU through a conventional loan path, depending on borrower, property, and lender requirements.

This renovation mortgage allows eligible borrowers to finance renovation costs through a single mortgage. It may be relevant for homeowners or buyers who want to improve a property, customize living space, or support multigenerational living through renovation financing.

For eligible Connecticut homebuyers, CHFA renovation loan programs may help combine the purchase price of a home and renovation costs into one mortgage. This is more relevant for buyers purchasing a property than for every existing homeowner, but it belongs on the list because it is Connecticut-specific and may apply to certain renovation-based ADU scenarios.

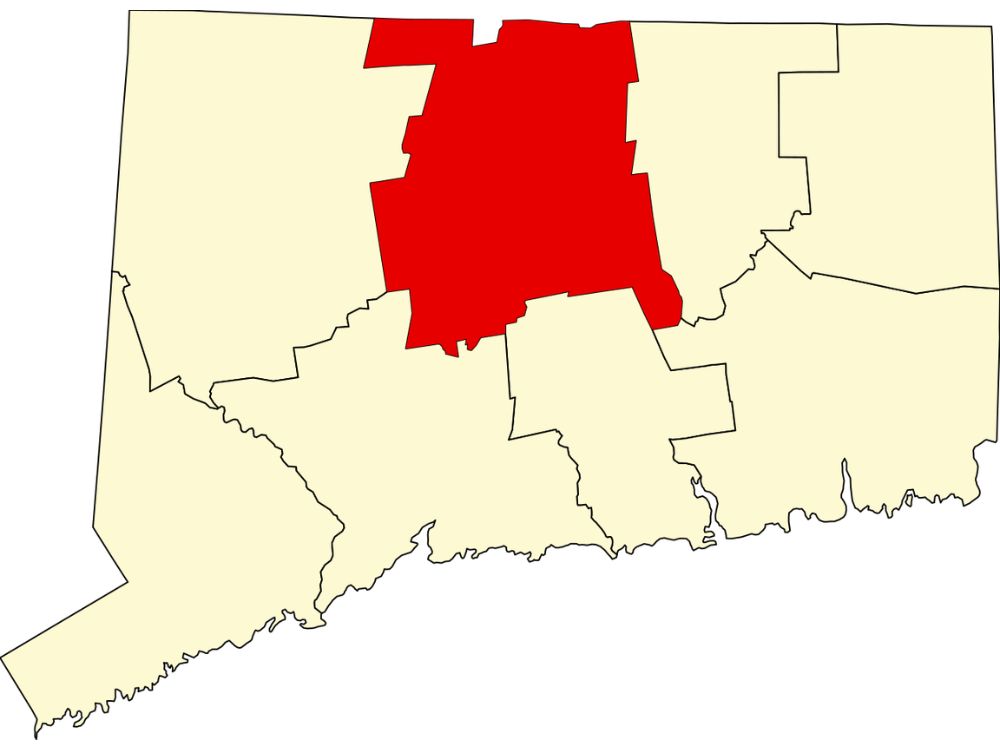

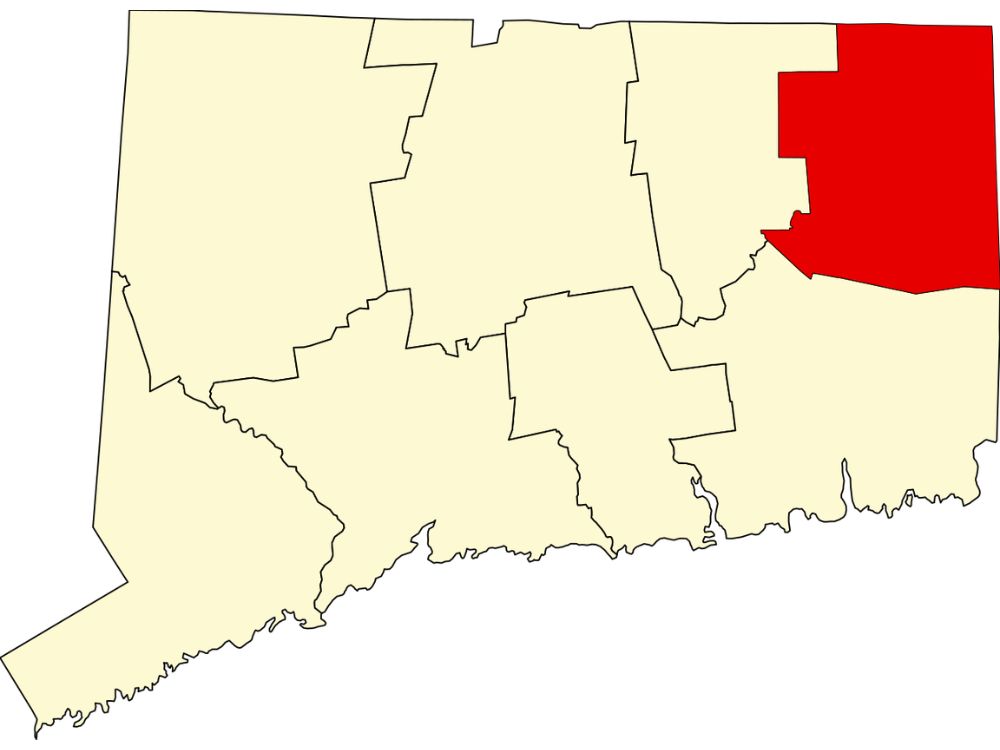

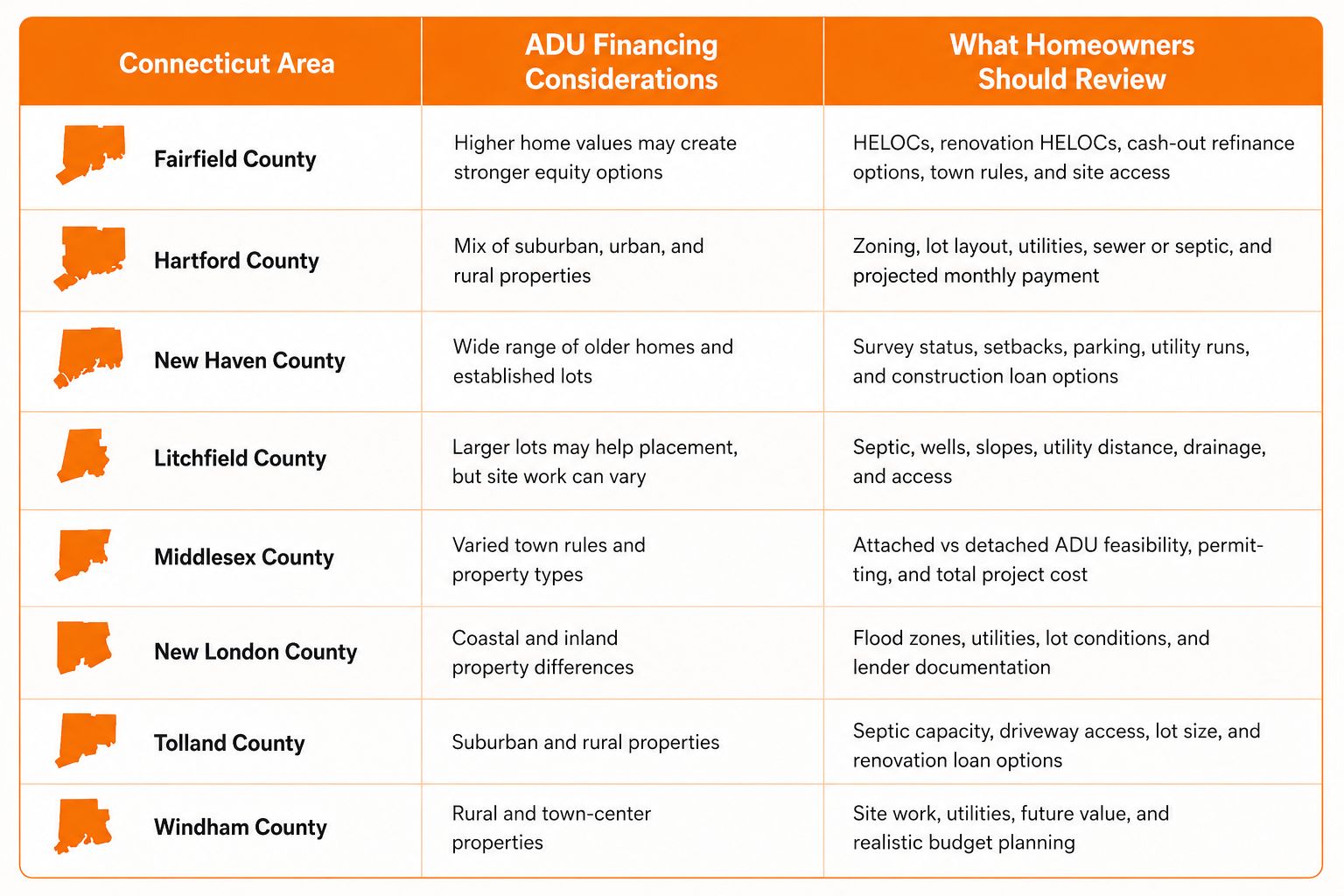

ADU Financing Considerations by Connecticut County

Contemporary Tiny Homes serves homeowners across the state of Connecticut in towns where ADUs can be built. Because each municipality may apply its own requirements, a financing conversation should be paired with an ADU feasibility review. A loan approval is helpful, but it does not answer where the ADU can go, what your town allows, or what site conditions may add to the cost.

How Much Does It Cost to Build and Finance an ADU?

ADU cost is one of the most important questions homeowners ask before choosing a financing strategy. In Connecticut, many custom ADU projects fall in the $150,000 to $300,000+ range, depending on size, layout, finish level, site work, utility runs, septic or sewer connection, electrical needs, permitting, and design requirements.

A smaller garage conversion or interior ADU may cost less than a new detached backyard ADU. A detached custom ADU with a foundation, long trenching distance, septic upgrades, premium finishes, accessibility features, or difficult site access may cost more.

Use Our Loan Calculator to See Sample monthly payments

For a rental ADU, compare the monthly payment with projected rent, vacancy, maintenance, taxes, insurance, and reserves. For a family ADU, the return may be less about rent and more about keeping family close, avoiding another property purchase, creating a one-level place for a parent, or preserving long-term flexibility.

How to Qualify for ADU Financing

Most ADU financing options look at a mix of borrower strength, property value, and project details.

Credit score expectations

Requirements vary by lender and loan type. Stronger credit can improve your options, but some construction, renovation, secured, or partner lending programs may have different requirements.

Equity requirements

HELOCs are usually based on current equity. Renovation HELOCs and ADU construction loans may consider the property’s future value after the ADU is complete.

Debt-to-income (DTI)

Lenders use DTI to compare your monthly debt payments with your monthly income. This helps determine whether the new ADU payment is manageable.

Using projected rental income

If the ADU will be rented, some lenders may consider projected rental income. This usually requires documentation, appraisal support, or lender-specific underwriting.

Project documentation

You may need a project estimate, builder scope, plans, appraisal, permit information, or draw schedule, depending on the financing option.

Property feasibility

Even if you qualify financially, your property still needs to support the ADU. Zoning, setbacks, septic, utilities, wetlands, surveys, and access can all affect the final plan.

Best Strategy for Financing an ADU

High equity homeowner: HELOC or renovation HELOC

If you have strong equity, a HELOC may give you flexible access to funds without refinancing your primary mortgage. If your current equity is not enough, a renovation HELOC may help by considering post-construction value.

Low equity homeowner: Construction loan or renovation loan

If you do not have enough current equity, an ADU construction loan may be a better fit. This option may require more documentation, but it can help bridge the gap when the completed ADU is expected to increase property value.

Investor: Rental-based strategy

If your ADU is primarily for rental income, focus on the relationship between projected rent and the monthly financing payment. Include vacancy, reserves, taxes, insurance, maintenance, and local rental rules in the math.

One family wanted to build an ADU for an aging mother, but they needed to complete the ADU before selling her home. A renovation HELOC allowed them to borrow against the property’s future post-construction value, build first, then use the home sale proceeds to pay the balance down. For homeowners who think they cannot finance an ADU, it is always worth discussing options before giving up on the project.The solution was a renovation HELOC against the daughter’s property. Because a renovation HELOC can factor in the property’s future post-construction value, the family was able to move forward with the ADU before listing the mother’s home. Once the home was sold, the proceeds were used to pay down the HELOC, leaving a smaller balance that could be paid over time. For homeowners who think they may not be able to finance an ADU, it is always worth discussing the options. Even if now is not the right time, it is important to understand the actionable steps that can put you in a position to build in the future.

ADU Financing Mistakes to Avoid

Choosing the wrong loan type

A HELOC, renovation HELOC, construction loan, and cash-out refinance each solve a different problem. The right option depends on equity, timeline, project scope, and repayment plan.

Underestimating costs

A starting price is not the same as an all-in project budget. Make sure you understand what is included, what is not included, and what property conditions could add cost.

Ignoring zoning delays

Your Connecticut town may have rules about size, setbacks, parking, attached vs detached ADUs, owner occupancy, and permitting. Financing should be paired with an early feasibility review.

Overleveraging equity

Using equity can be smart, but borrowing the maximum amount available may leave too little room for rate changes, site surprises, or final finish decisions.

Step-by-Step: How to Finance an ADU in Connecticut

Learn how to finance an ADU in Connecticut with a clear step-by-step process covering home equity, total ADU project cost, HELOCs, renovation HELOCs, construction loans, refinance options, lender pre-approval, ADU permits, builder planning, and the final close and build stage. This guide helps Connecticut homeowners understand ADU financing, ADU construction costs, and the key steps to prepare for an accessory dwelling unit project with more clarity and fewer surprises.

Tools & Resources

ADU Loan Calculator - Payment Estimator

Explore Your Budget with Our Loan Calculator. Curious about how much your ADU will cost? Use our interactive ADU Loan Calculator to estimate monthly payments based on different loan amounts, interest rates, and repayment terms.

ADU cost calculator

Use the ADU cost calculator to estimate your likely project range based on size, build type, finishes, utilities, and property conditions.

CALCULATOR COMING SOON!

Return-on-Investment (ROI) calculator

Use the ROI calculator to compare projected rent, monthly financing payment, long-term equity growth, and future use cases.

Frequently Asked ADU Financing Questions

Get Answers to Your Questions About Design, Construction, and More

What is the best way to finance an ADU?

The best way to finance an ADU depends on your equity, credit, income, project cost, and use case. High-equity homeowners may use a HELOC. Lower-equity homeowners may explore construction loans or renovation HELOCs. Rental-focused buyers may look for options that consider projected rent.

Can you finance an ADU with little or no equity?

Yes! Besides HELOCs, our lenders offer secured and unsecured personal loans as well as construction loans.

Are there ADU grants in Connecticut?

There is not one universal Connecticut ADU grant for every homeowner. However, financing programs, local incentives, and housing resources can change. It is worth reviewing current options with a lender or ADU specialist before deciding there is no help available.

How much can I borrow for an ADU?

The amount you can borrow depends on your lender, credit profile, income, DTI, home equity, loan type, and project scope. Some options use current value, while renovation and construction products may consider future post-construction value.

Can rental income help qualify?

In some cases, yes. Certain lenders may consider projected ADU rental income if it is properly documented and supported by underwriting or appraisal requirements.

Is ADU financing different from a home addition loan?

Yes. ADU financing may be treated differently because an ADU can function as an independent living space with sleeping, cooking, and bathroom facilities.

What credit score do I need for ADU financing?

Credit score requirements vary by lender and loan type. In general, stronger credit creates more options, but some secured, renovation, construction, and partner financing options may have different standards.

What permits and approvals are needed to build a Custom ADU?

You’ll need zoning, building, electrical, and plumbing permits, which vary by municipality. We'll work to obtain those for you from your town's authorities having jurisdiction.

What is the process for building a Custom ADU?

Our process includes initial consultation, custom design, permitting, and construction—all managed by our experienced team. Learn more on our Custom ADU page.

Can I leverage the equity from a different property I own?

Yes! HELOCs are very flexible. You can finance your ADU by getting a HELOC on a property at a different address.

Can I use part of the HELOC funding for other things besides the ADU construction?

Yes! Besides HELOCs, our lenders offer secured and unsecured personal loans as well as construction loans.

Yes! HELOCs are very flexible. You can get additional funding for furniture, moving expenses, or even expenses that are unrelated to the ADU, such as pending medical bills.

Final Thoughts: Is ADU Financing Worth It?

ADU financing can be worth it when the project solves a real need and the monthly payment fits the plan.

For one Connecticut homeowner, the value may be rental income. For another, it may be a one-level place for a parent, a private in-law suite, a future downsizing option, or a way to make better use of land they already own.

The right ADU financing option can help you move sooner, but the best decisions come from clear numbers. Before you commit, find out what is possible on your property, what the full project may cost, which financing options fit your situation, and what could affect the budget later.

At Contemporary Tiny Homes, we review feasibility, cost, financing, and next steps with Connecticut homeowners in plain language so they can make a confident decision.

Ready to Design Your Perfect Custom ADU?

Take the first step toward creating your Custom ADU! Schedule a free consultation today, and let our ADU experts help you design the ideal solution tailored to your space and lifestyle.

Looking For Something Different? Explore Our ADU Models

Studio ADUs are ideal for minimalist living,

combining functionality and simplicity into a compact design. With an open floor plan, a studio ADU maximizes every inch, making it an ideal solution for individuals seeking a cozy retreat or an affordable living solution.

2-bedroom ADUs are perfect for small families or those who need a little extra space. Two separate bedrooms offer flexibility for guests, children, or a home office. These homes provide all the functionality of a traditional house in a much smaller footprint.

Email [email protected]

Phone 860-846-4100

Copyright 2026. All rights reserved. Norwalk, CT

Connecticut's New Home Construction Contractor License: #NHC.0017654

EPA Lead-Safe Certified NAT-F269966-1